As more NRIs invest in Indian real estate, understanding taxation has become an essential part of wealth planning. Here’s how to approach it with clarity and a long-term perspective.

For many NRIs, purchasing a home in India is more than just expanding their investment portfolio. It’s about staying connected to your roots, to be able to buy a home, create a legacy for future generations, or to be able to own a place to be able to return to. However it’s also becoming a strategic financial decision, with India’s luxury real estate market attracting global interest far and wide.

Yet while potential homeowners often spend time evaluating locations, developers, and appreciation potential, taxation tends to receive attention much later in the process. However, understanding the NRI Property Tax in India isn’t just about being compliant. Instead, it helps you structure your investment more effectively, manage cash flows better, and avoid unexpected costs down the line.

Here is what every NRI Investor should know before purchasing a property in India:

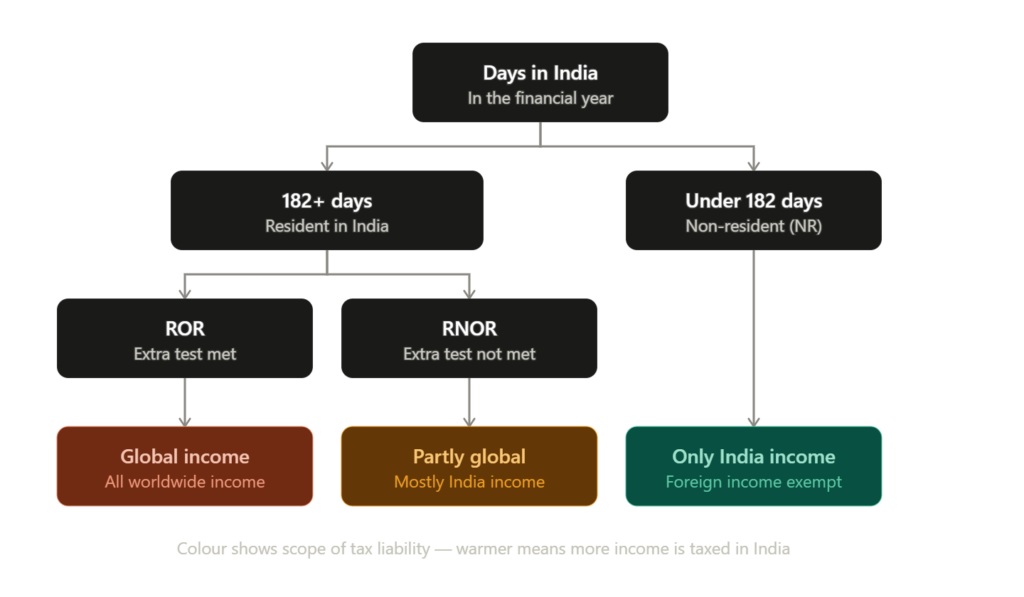

Understanding Your Residential Status

Before considering the Tax implications of buying a home or a property, it is important to understand your residential status under the Indian Income Tax Laws. Whether you are classified as a Non-Resident Indian (NRI), Resident, or Resident but Not Ordinarily Resident (RNOR) determines how your income will be taxed.

Your residential status isnt based on your passport or citizenship, but on the actual number of days you spend in India during a financial year. This classification is what forms the basis for NRI Real Estate Taxation in India, helping influence everything from rental income to capital gains.

Taxes at the Time of Purchase: More Simple Than You Think

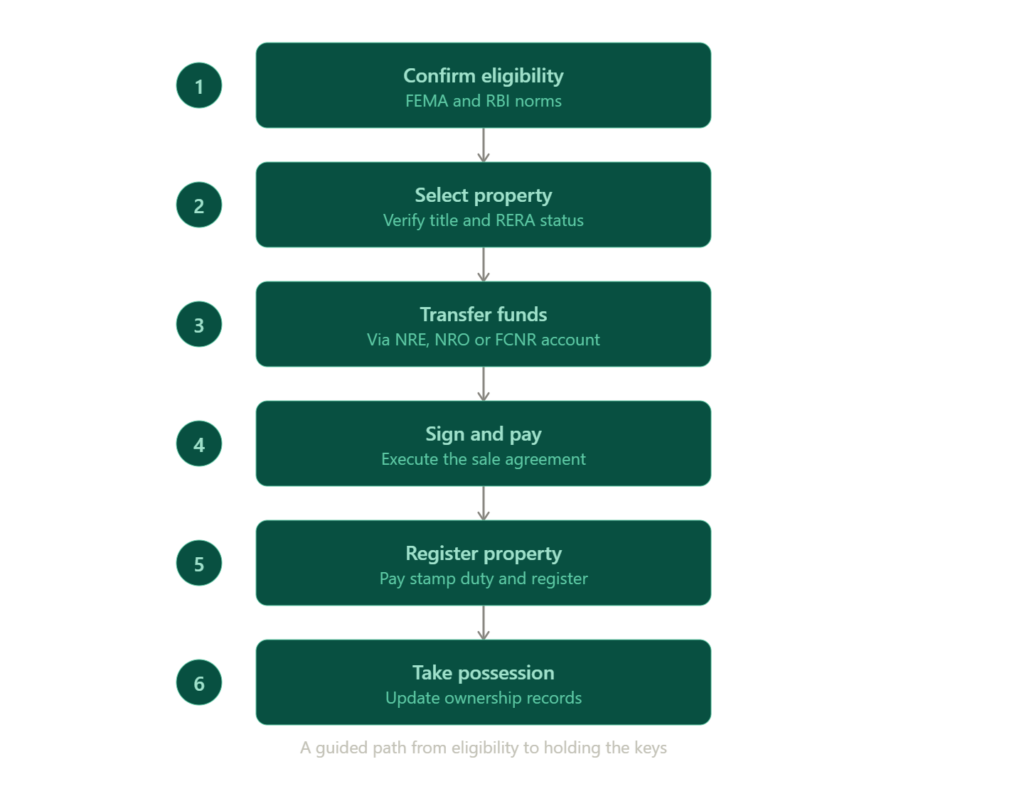

One of the biggest misconceptions is that NRIs face significantly higher taxes when purchasing a property in India. But in reality, the process is similar to that of resident buyers. Stamp duty and registration charges are levied according to the state in which the property is based, and these costs generally remain the same for NRIs and Indian residents. While there are no special tax concessions available purely because you are an NRI. Property purchases must comply with applicable FEMA Rules for Property in India, particularly regarding eligible property types and funding sources.

Most buyers finance their purchases through NRE or NRO accounts, making it easier to manage future transactions, including rental income and repatriation. The purchase stage is relatively straightforward. It’s what happens after you become an owner that requires more thoughtful consideration.

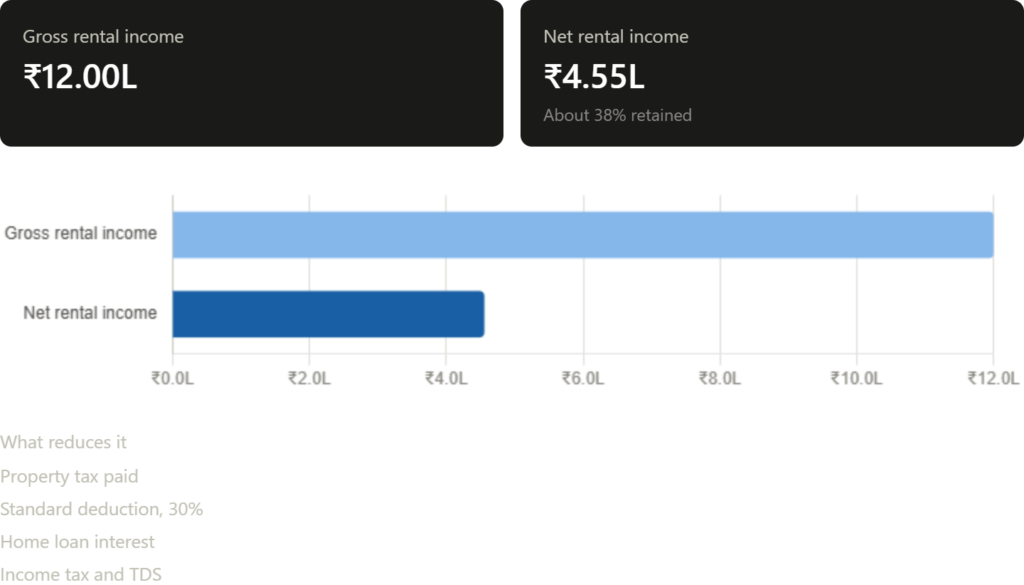

Rental Income: Understanding Your Real Returns

If you are purchasing a home as an investment, real income becomes an important part of your financial equation. Under Indian Tax Laws, Rental Income Tax for NRIs in India is applicable on income earned from property located in India. In many cases, tenants are required to deduct Tax Deducted at Source (TDS) before making rental payments to an NRI landlord.

However, your taxable income is not the same as your rental income. Eligible deductions, including municipal taxes, maintenance and home loan interest (where applicable), may help reduce your taxable liability. Filing an income tax return in India is generally required to claim these benefits to determine the accurate final tax payable. And for many investors, the focus tends to be on rental yield, and in reality, understanding your post-tax income provides a much clearer picture of an asset’s long-term performance.

Selling Your Property: Planning right for Capital Gains

The tax implications become more pertinent when you decide to sell. If the home is sold within two years of the purchase. Any gains are generally treated as Short-Term Capital Gains, which are taxed according to the applicable income tax slab.

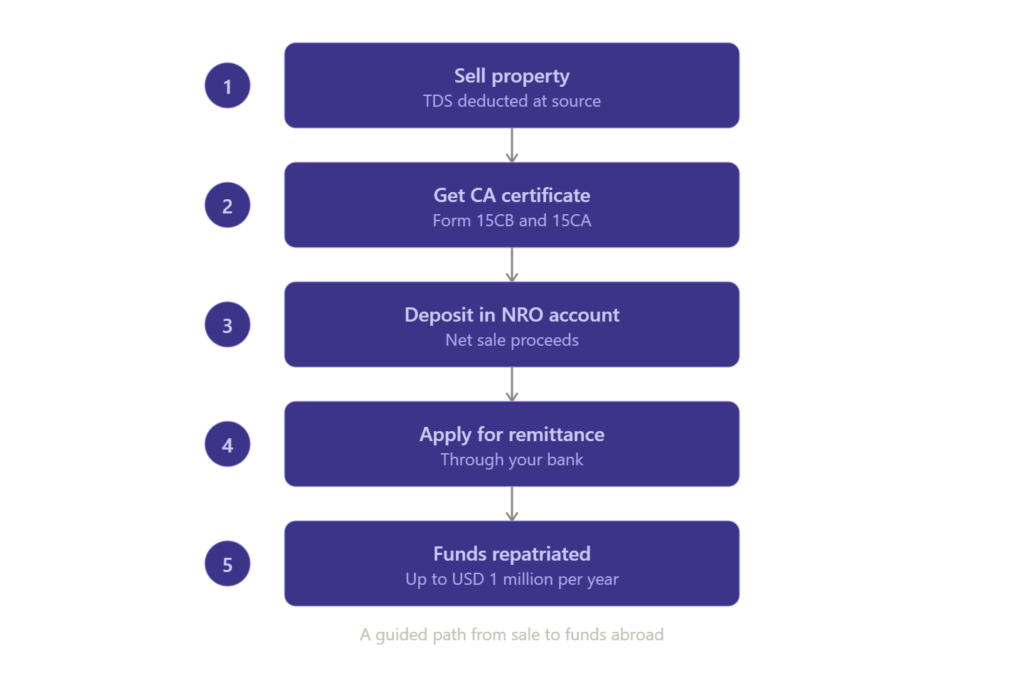

Properties held for more than two years qualify for Long-Term Capital Gains, which are currently taxed at applicable rates under prevailing tax laws, subject to available exemptions and provisions. An important aspect many sellers overlook is TDS on property sale for NRIs. Unlike transactions between Indian residents, the buyer is legally liable for deducting TDS before paying the seller. The applicable TDS amount can be substantial, making planning in advance essential for managing accurate cash flows.

Understanding the Capital Gains Tax on NRI property well before a sale helps avoid surprises and ensures smoother transactions.

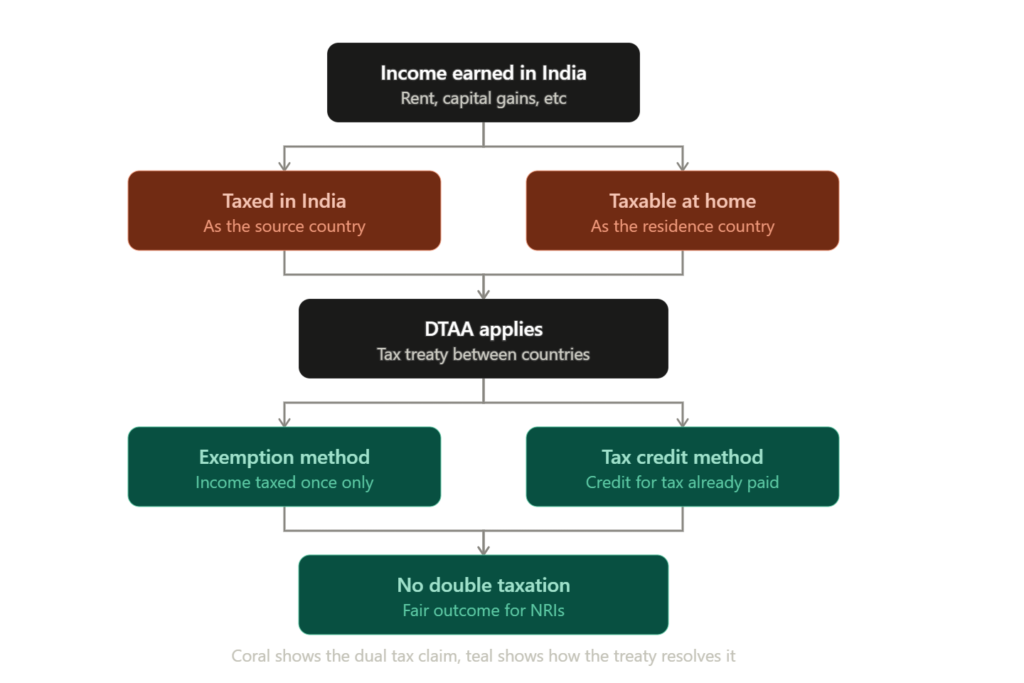

Double Taxation Does Not Mean Paying Twice

The most common concern among overseas investors is whether they will be taxed in India and their current country of residence. And this answer entirely depends on the Double Taxation Avoidance Agreement (DTAA) between India and the country you currently reside in. These agreements are designed to prevent the same income from being taxed twice; this can be either through tax credits or exemptions depending on the applicable treaty.

Tax laws vary across countries and jurisdictions. It’s worth seeking professional advice to understand how Indian property income fits into your global tax position. The objective here isnt to avoid tax but rather to ensure you are paying only what is required.

Repatriating Your Money: Plan Early

Whether you are earning rental income or selling your property, moving funds overseas is an important consideration. India allows NRIs to repatriate eligible rental income and sale process, subject to RBI regulations and prescribed documentation. These rules often involve some amount of paperwork, bank certifications, tax compliance, and a few more.

While the process is in place, planning for repatriation should be done at the time of purchase, not after the sale, which helps simplify future transactions considerably.

Beyond the Taxes

Tax efficiency is an important aspect of property ownership, but this is not the primary reason for investing. The strongest real-estate conversations continue to be driven by enduring basics:

- Location

- Design

- Quality of construction

- Long-term demand

- Ownership experience

A well-located and thoughtfully designed home is far more likely to deliver sustainable value than one chosen purely for perceived value and tax advantages. Similarly, managed homes often simplify several aspects of ownership, from maintaining documentation and managing tenants to streamlining rental administration. And for NRIs living overseas, professional management can make ownership significantly easier and reduce operational complexity.

Common Mistakes NRIs Can Avoid

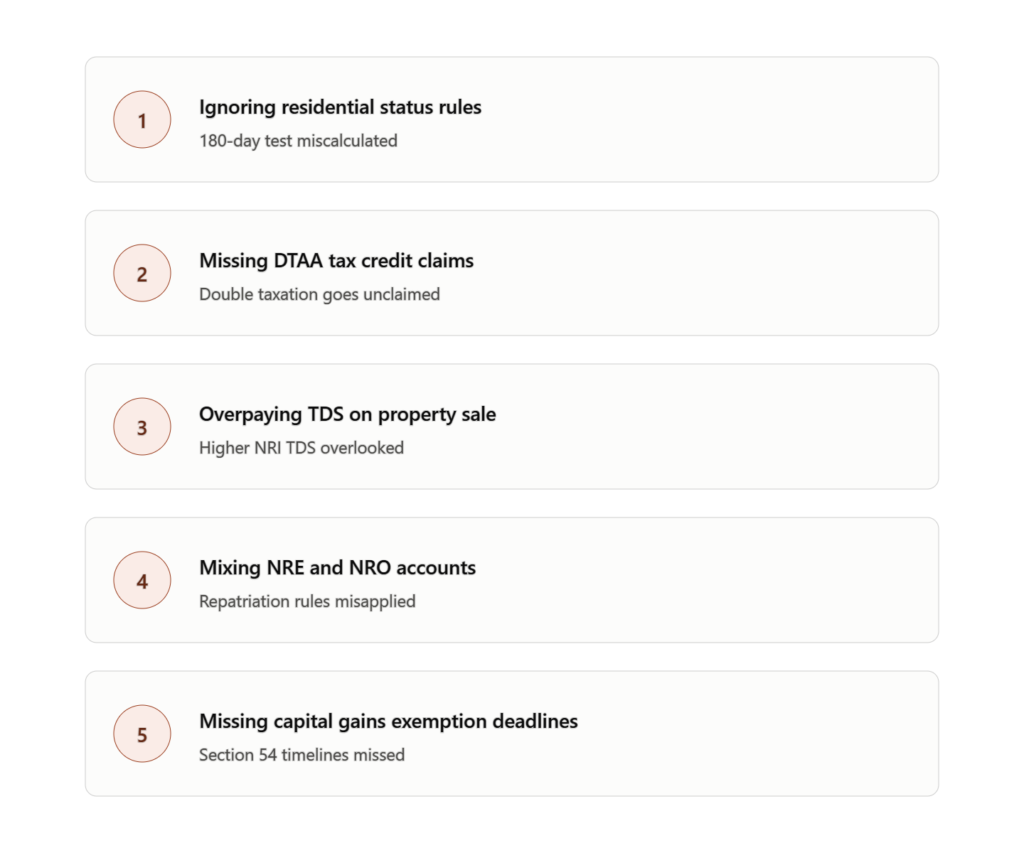

While India’s tax framework is well established, a few mistakes can cause unnecessary complications. Some investors underestimate the impact of TDS when selling, while others don’t account for post-tax rental income when evaluating returns. Many also postpone discussions around repatriation until the stage of sale, or fail to explore the benefits available under applicable DTAA’s

Investing With Clarity

Indian luxury real estate continues to present compelling opportunities for NRIs looking for financial growth and a meaningful connection to home. Understanding the tax implications for NRI investing in India is an essential part of your journey. Not because it should dictate your decisions, but because it helps you make them with greater confidence.

When viewed as a part of the broader image – Wealth planning strategy, taxes become one element of thoughtful ownership alongside location, asset quality, long-term appreciation, and ease of management. The goal isn’t simply to minimise tax; it’s to build an investment that continues creating value for years to come; financially, personally and across generations.