From rising property values in sought-after destinations to inflation-linked rental income, holiday homes are emerging as a compelling real estate hedge against inflation in India.

Inflation is no longer an abstract statistic; it quietly reduces the purchasing power and reshapes how affluent individuals think about wealth. Traditional cash savings and low-yield fixed instruments routinely lag price growth. Helping prompt HNIs and UHNIs in India to re-evaluate tangible assets that combine capital preservation with utility. Against this backdrop, the holiday home emerges as a hybrid proposition: part lifestyle, part asset. But does a second home genuinely serve as an effective hedge against inflation in India, or is its value largely sentimental? The answer depends on selection, management, and how the asset is used.

What ‘’Hedging against inflation’’ means in practice.

To hedge against inflation is to hold assets whose real value (or income streams) rises at least as fast as the general price level. Common examples include gold, equities, and real estate. Each behaves differently: gold preserves nominal value but yields no income; equities can outpace inflation over the long term but are volatile; real estate historically offers both appreciation and an income stream. A holiday home falls within the real estate category but must be understood on its own terms: it is a physical, usable asset whose value is shaped by location, design, and the marketplace for leisure stays as much as by macroeconomic factors.

How Holiday Homes Help Function as an Inflation Hedge

- Capital appreciation over time

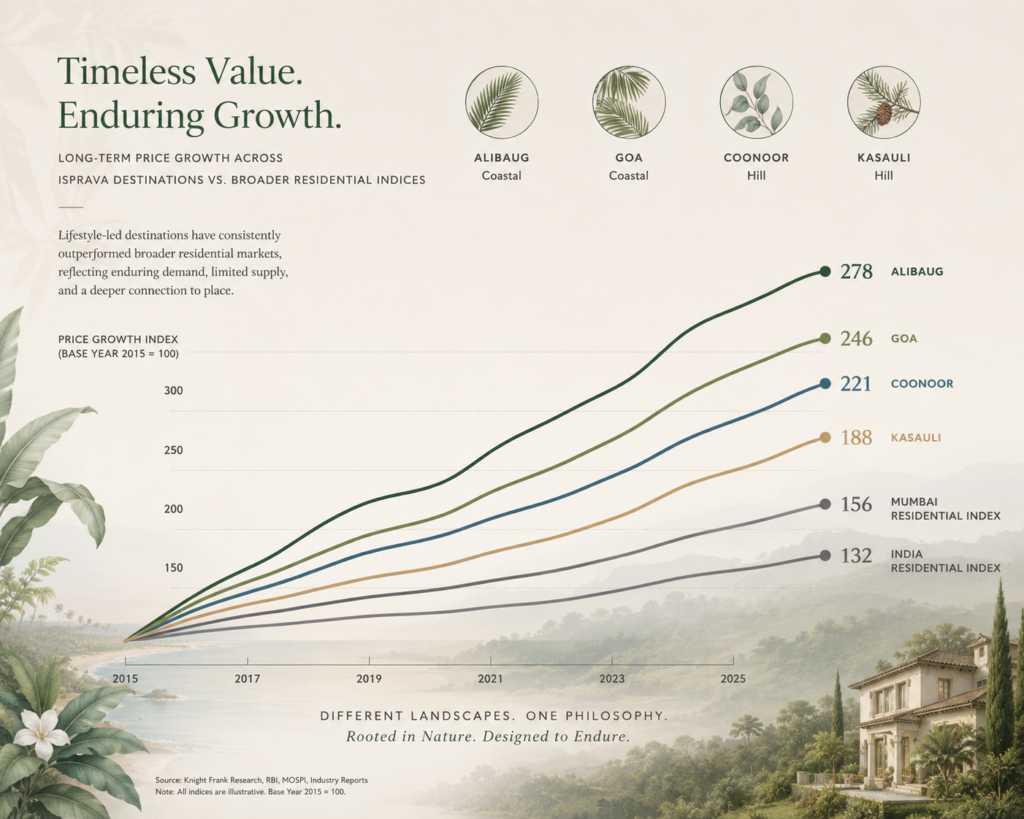

Land scarcity, planning constraints, and growing domestic demand have elevated the long-term prospects of well-located holiday markets in India. Picture coastal and hill stations micro-markets. Homes in these well-fringed pockets benefit from constrained supply and lifestyle-led demand, which helps sustain price growth above national averages. Crucially, appreciation is not automatic: it is accrued to homes that are resilient in micro-locations with curated design styles and maintenance.

Suggest visual: chart comparing long‑term price growth across coastal/ hill holiday micro‑markets versus broader residential indices.

- Rental Income that helps adjust to inflation

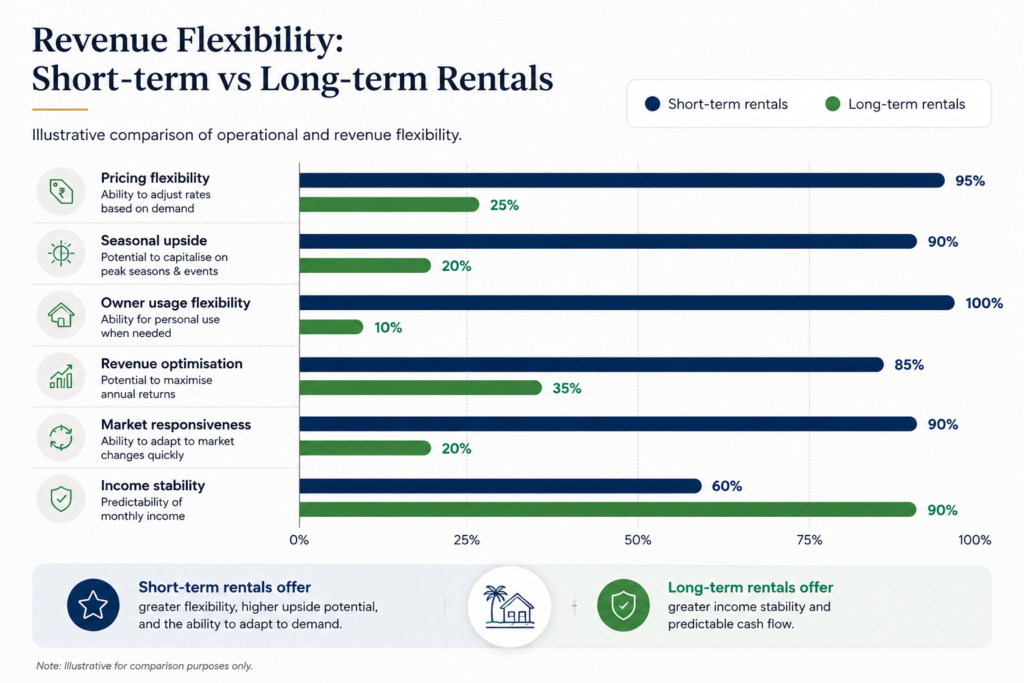

Unlike traditional gold, a holiday home can help generate recurring cash flow. Short-term rental models (Daily/Weekly) allow dynamic pricing that helps track more closely seasonal demand and inflationary pressures than fixed long-term leases. In periods of rising prices, per-night rates and therefore gross rental revenue can be adjusted quickly. Preserving real income, an effective property management ecosystem, yield optimization, and a curated guest experience are the levers for a seamless operation.

- Dual Benefit: Use & Income

A holiday home is unique among inflation hedges in offering personal utility alongside potential income. This duality helps the owner capture both experiential value: family practices, restorative escapes, and financial returns. When evaluated as an asset, the combined metric of lifestyle value plus net yield make holiday homes a more compelling and emotionally defensible store of wealth.

Why Luxury Holiday Homes Often Outperform Standard Real Estate

Luxurious holiday properties tend to outperform for three reasons:

- Pricing power: Design, provenance, and low‑density planning allow higher per‑night rates and resilient capital values.

- Deliverable experience: Properties that are curated, well‑managed, and authentic attract repeat demand and premium guests.

- Micro‑market insulation: High‑quality, secluded estates preserve desirability even when broader markets fluctuate.

And in simple words, a design-forward, professionally managed holiday home in a strong micro-market is more likely to deliver both inflation-linked income and durable capital appreciation than a generic residential property.

Comparing holiday homes with other inflation hedges

- Gold: Stable nominal store of value, no yield.

- Equities: Best historical real returns, but with short‑term volatility and behavioral risks.

- Urban residential property: Predictable but often low rental yields (typically 2–4%), and tenant dynamics can lag inflation.

- Holiday homes: Potentially higher yields (subject to market), immediate experiential value, and, when managed, dynamic pricing that responds to inflation.

This helps Holiday Homes turn into a hybrid hedge: they offer income potential comparable to higher-yield assets and the tangibility and utility that reinforce long-term value retention.

The Role of Short-Term Rentals in beating Inflation

The modern short-term rental ecosystem: platform distribution, professional management, flexible pricing, and ancillary services. This enables holiday homes to capture seasonal premiums and react quickly to market changes. Whereas long-term leases are locked into annual escalations, short-term pricing can be updated daily, enabling real-time adjustments for cost increases and demand spikes. For owners, this flexibility is key by which the holiday homes can act as an effective inflation hedge.

What determines whether a holiday home truly hedges inflation? Not all holiday homes are equal. The difference between protection and exposure hinges on:

- Micro‑location: Accessibility, natural appeal, and tourism infrastructure.

- Quality of Design and Build: Timelessness, materiality, and maintenance cost profile.

- Management: Professional operations, dynamic pricing, and marketing.

- Legal clarity: Clear title, regulations for short‑term rentals, and tax compliance.

- Demand consistency: Year‑round vs highly seasonal markets.

Absent these factors, owners face illiquidity, high running costs, and income volatility that can erode any inflation protection.

Risks and the Balanced View

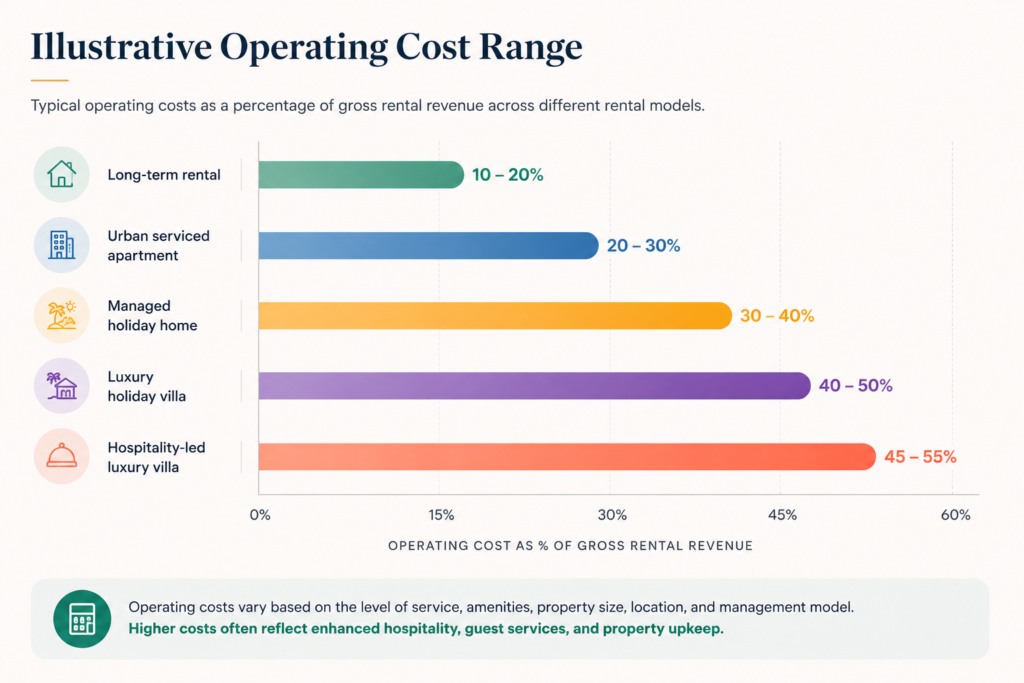

A candid assessment recognises real drawbacks: holiday homes are less liquid than equities; they incur ongoing maintenance and management costs; income can be seasonal; and overpaying in overheated markets undermines returns. The key is selection; buying into well‑curated, low‑density developments in resilient micro‑markets and pairing ownership with professional management reduces many of these risks.

An Isprava Perspective: Design and Stewardship Matter

From a preservation and returns standpoint, design‑led, low‑density developments that prioritise craft, contextual architecture, and thoughtful landscaping retain value better. Professional management ecosystem: guest curation, maintenance regimes, and brand consistency help turn a home into a reliable income generator. For owners seeking both lifestyle and wealth preservation, this integrated approach converts an emotional purchase into a disciplined long‑term asset.

Beyond Returns: A Smarter Way to Store Wealth

A holiday home can be an effective hedge against inflation in India, but only when treated as more than a sentimental purchase. The actual advantage lies in assets that earn (inflation‑linked rental income), appreciate (select micro‑markets, scarcity, and design), and enrich (personal utility and legacy). For affluent buyers, the smarter approach blends rigorous market selection, design integrity, and professional stewardship. In an era of persistent inflation, assets that combine economic resilience with lived experience, not just spreadsheets, help offer the most durable form of preservation.